The Size Credit Orderbook: A Giga-brain’s Delight

AKA: When fixed rates become better than fixed

Fixed rates are great because you can lock in your cost of borrowing, for a known cost of capital.

But how can they get even better?

If I’m trying to really giga-brain it, when I open a Size Credit loan to borrow, it is a bit like I am taking an interest rate call option. I have a MAXIMUM amount of interest I have agreed to pay for a specific term and amount, but a lot can happen throughout that term. For example, if the rates subsequently skyrocket I will gladly ride out my term and pay that low interest rate that I locked in at my interest rate “strike price”.

But how else can this play out?

Sure, I can ride out my full term and pay that full interest. But if I’m being thoughtful, I can actually trade that credit position against the orderbook. Another way to say this is “I can speculate on the outlook of rates, how that compares to the rate I already have, and the way the market is pricing rates now and in the future.”

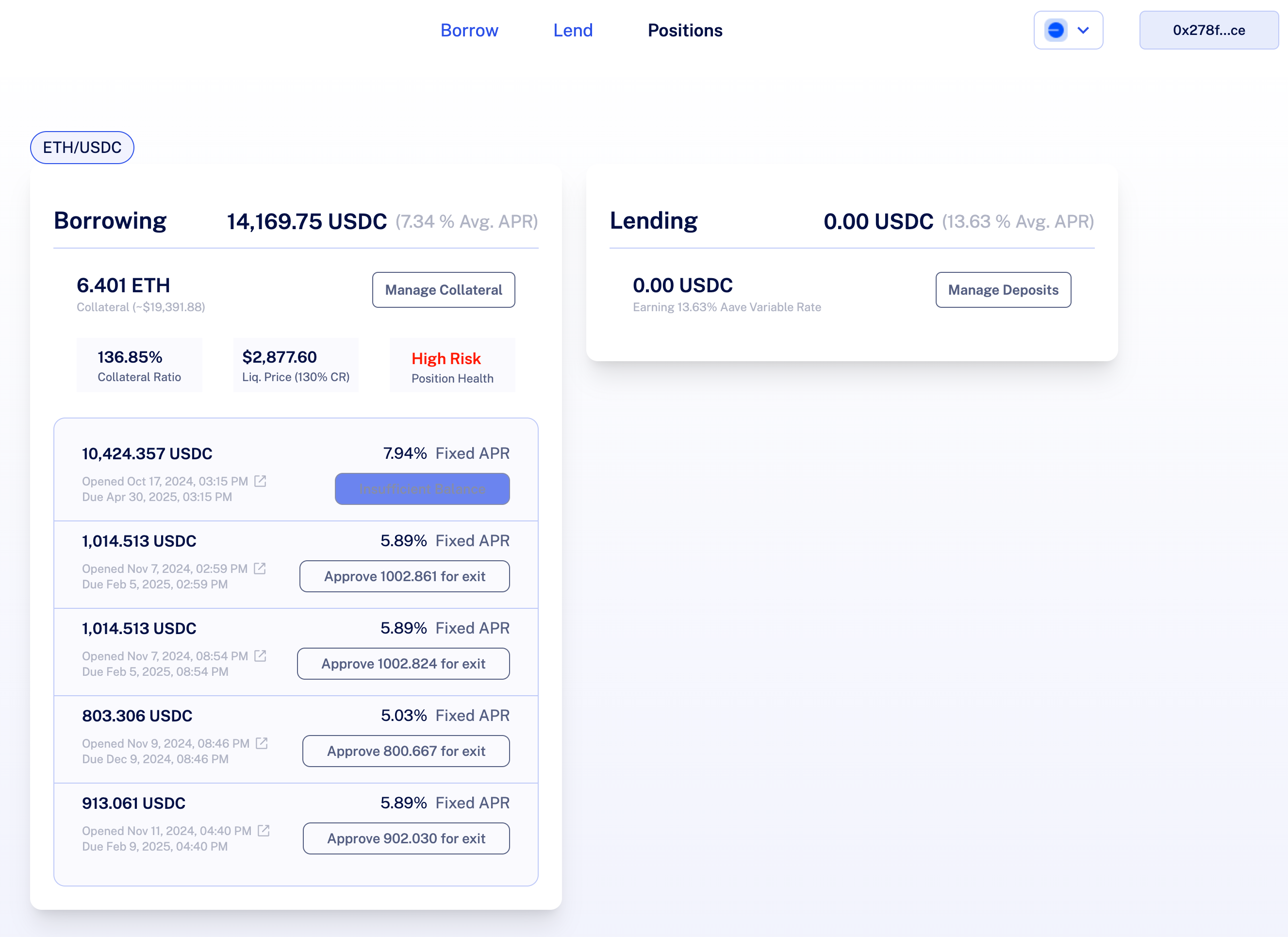

Great - that all sounds super heady and feels very giga-brain-y, but what does it look like practically? Here is a smattering of borrow positions I’ve opened on Size Credit with a variety of fixed rates and maturities:

Not bad, right? Considering that long BTC and ETH perps on CeFi exchanges are costing 20-60% APRs to be long, locking in all single digit fixed rates felt pretty good.

But let’s look a little more closely at the exit options on some of these. What we’re looking at is the ability to exit this loan back into the Size Credit orderbook instantly, and the price at which these could be exited. By matching with someone else who is already a willing borrower, I can get out of my obligation by repaying just the difference that they require to be willing to take the loan over, rather than paying the full term amount. Then I am out of the position, and they now have the smart contract obligation on the loan term.

We should dive deeper into that second to last loan in that screenshot:

The notional size of this loan was $800, with $3.30 and change in notional interest for the listed term (Nov 7 to Dec 9) to arrive at a 5.03% Fixed APR. If this was just a linear rate, my interest would be accruing at a rate of 1/28 for the 28 days of the loan term. But Size is a credit market, not just a static linear-rate loan machine. That means that although I have agreed to pay 5.03% for the full term of the loan, if I wanted to exit my loan right now then my real interest rate is simply the best rate at which I can find someone else who is willing to buy me out of my loan.

What this means is that especially if rates skyrocket, thinking about my Size loan as a “rate call option” makes a lot of sense. I’ve committed to a 5.03% maximum fixed rate, but if I’m clever I could potentially get my effective interest rate down to 4%, 2%, or even ZERO percent. If today willing borrowers are willing to pay twice as much interest as when I opened my loan, then even if I am already 3 months into a 6 month loan there is a chance I could find a willing borrower to pay my ENTIRE term interest on the 6 month loan for the opportunity to hold it for 3 months - meaning that I got a 3 month loan for zero interest. And it’s worth noting that this opportunity could persist all the way to maturity; because rather than isolating liquidity to specific maturities like end of quarter or end of year, Size Credit unifies liquidities across any and all maturities. This means that there will likely be exit liquidity throughout the life of my loan, rather than any set-maturity products where liquidity naturally dwindles the closer it gets to expiration.

Now we have to do a TINY bit of math. I like to say that in DeFi, math is alpha - because degens hate to do math. My $800 principal will cost me $3.30 if held to maturity, or 0.41% total interest - this is my fixed 5.03% APR if I annualize the loan duration. Cool, that all checks out. But if I wanted to dump it today I can do that for $800.67… or just $0.67 on top of my principal. This comes out to just 0.08% total interest on my loan, or just 0.013% a day. So while I locked in a 5.03% rate with that “call option” mindset, I could exit right now at an effective rate of 4.75% for the term of the loan. To put that more plainly, I just shaved a quarter percent off my fixed rate, and I’m getting out early.

I know what you’re thinking - a quarter of percent is hardly exciting, especially in the context of DeFi where APRs soar into 4 digits, 5 digits and beyond. And you’re not wrong; 25bps is not exciting, to degens. But you know who it is exciting to? Prop trading firms. Private Credit funds. Big, quiet arb funds. THE quote-unquote Liquidity. Folks like TwoSigma, Citadel, Millenium.

If we really want institutional capital to enter DeFi, I can assure you it will never be to buy speculative and risky tokens named after dogs or cats or deceased squirrels. It will be because they see the opportunity to take things they are already very good at and comfortable with, like trading interest rates, durations, and order books on deeply liquid dollar markets. Trades they can execute in Size - pun fully intended. And THAT is why regardless of whatever animal is up 79,000% in the last 24hrs, I’m still more bullish on these 25bps.